How to Support Your Parents Financially Without Going Broke | Palm Beach County, Florida, Save money on Prescription drugs is easy The RX Solutions is the right choice.

What to Do if Your Aging Parents Are Going Broke

This is part of a series of stories offering help with “Hot Topics“ — tricky family conversations that have real financial impact.

It’s a money leak that no one’s talking about: Nearly one in four Americans helps support a parent financially, according to a Care.com survey. But most families don’t discuss the issue — or the dollars involved — until a health or other crisis arises, says Jody Gastfriend, vice president of senior care at Care.com.

Without a game plan, you could wind up footing large unexpected bills, harming your own finances, and providing lesser-quality care for your parents. To be more prepared, address the issue before it’s an emergency.

PAIN POINT

Among families who help support parents financially, a third spend more than $5,000 a year, and another 19% dole out more than $10,000 a year.

PREP WORK

To be able to have a practical conversation with your spouse, you need to understand what assets and insurance coverage your parents already possess, and what their actual needs would be. If one parent were to require extra care at home, for instance, a home health aide would cost $3,861 a month on average, according to a report by Genworth. You “can’t think about giving financial support until you know what degree of support is needed,” says Columbus, Ohio, financial planner Lisa Walls.

Talk to your parents about where they stand and how much planning they’ve done. Let them know that you want to be able to help if needed. Create a balance sheet with them to identify trouble spots and, if possible, areas to cut down spending.

OPENING LINE

“After hearing how much Virginia is spending to help out her folks, I started worrying about our own parents. I’m worried that they’re not going to be able to handle any expensive emergencies.”

Instead of waiting till the last minute, spark the conversation early by using a friend’s situation or a current event, without applying pressure or a deadline. Include both sets of parents, if applicable, when voicing your concerns. “Resentment can build when the talk is all about one parent,” says Indianapolis financial planner Michael Kalscheur.

TALKING POINTS

“I want to set aside some money in case our parents need help. I don’t want us to be scrambling should anything happen. How much do you think we could afford?”

The biggest mistake people make when helping parents is overextending themselves and derailing their own plans, says Cedar Rapids, Iowa, financial planner Derek Tharp. The best thing you can do: Prepare. You want to avoid being drained when a crisis arrives — and the best way to do so is to carve out an emergency support fund in advance.

Feeding this fund now will require some juggling with your many other financial priorities — but setting aside a small percentage each month will hurt less than facing a $5,000 lump sum. Work with a financial planner or review your budget yourself to see what, if any, spare income can be diverted for this purpose.

Understand how much you can set aside — and how much both sets of parents are likely to need, based on your conversations with them. Factor in some “what if” scenarios, says Walls: What would happen if one needed long-term nursing care, for instance? Or what if there was a sudden home repair emergency?

Knowing your financial limits in advance can help you avoid putting your own financial future at risk. And figuring out the potential costs can give you time to save up.

–––

“I think my folks will need help covering long-term care costs. If they do, I want to use some of the money we set aside to pay those bills directly. Does that make sense to you?”

NEXT STEPS

Set up a family team, recommends Walls. Talk with your parents, siblings, and spouse to determine who can take on separate caregiver roles — taking care of household chores, dispensing medication, paying bills — should your parents require extra help. Parents often need financial support because of a health care crisis, says Gastfriend, so discuss physical help as well as financial.

Draw up a financial plan that you could put in place as needed. It should incorporate all income streams: your parents’ own funds, yours, and contributions from other family members.

The goal is to have a clear road map for who will provide necessary care and how it will be paid for long before your family need it, as well as access to key financial documents. “It’s often decisions made earlier in life that set families up for the best outcomes,” says Tharp.

ONE FAMILY’S SOLUTION

“I recently had a discussion with a thirty-something client regarding his parents’ future care,” says Washington, DC financial planner Rachel Podnos. “In the end, we decided that his parents were good candidates for long-term care insurance, because they did not have the financial wherewithal to pay for their own care. One thing we discussed was him purchasing policies on his parents’ behalf and splitting the cost of the premiums with his siblings.”

Medication Assistance for Low Income

Are you uninsured, underinsured, or have Medicare prescription coverage and are having difficulty paying for your medications?

PRESCRIPTION ASSISTANCE IS AVAILABLE HERE! WE WILL WORK WITH YOU AND YOUR DOCTORS TO EXPEDITE THE APPROVAL PROCESS! WE ALSO ASSIST WITH YOUR REFILLS!

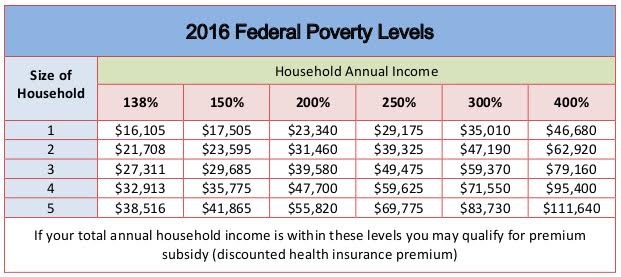

There are over 270 Patient Assistance Programs. Each Patient Assistance Program has different qualification guidelines. However if you meet the following three conditions you will more than likely qualify for these programs.

DEFINING ECONOMIC HARDSHIP

The exact definition of economic hardship varies with each Patient Assistance Program. Most Prescription Assistance Programs adhere to a formula related to the Federal Poverty guidelines. If your income is 200% below the Federal Poverty guidelines, then you will most likely qualify. The qualifying income levels for the most current year are outlined below.